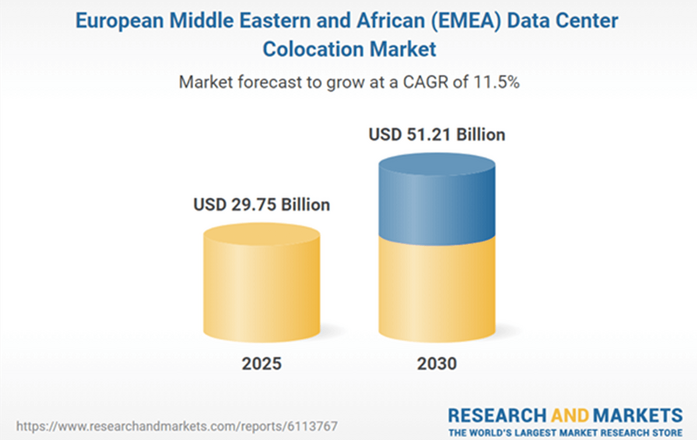

The European Middle East and Africa (EMEA) data center colocation market is expected to grow from USD 29.751 billion in 2025 to USD 51.208 billion in 2030, at a CAGR of 11.47%.

Hyperscale Demand and Digital Transformation

The increasing reliance on colocation services by hyperscale data center users, such as cloud providers and tech giants, is a primary growth driver. In 2023, major cloud providers like Microsoft and Google leased significant capacity in urban centers across Europe, boosting demand for scalable infrastructure. The Middle East and Africa are undergoing rapid digital transformation, fueled by the fourth industrial revolution, IoT, and smart city initiatives.

Industry Investments and Expansion

Colocation providers are actively expanding to meet rising demand. In February 2023, Data4 established a new data center in Hanau, Germany, on a former army barracks site, signaling robust investment in Western Europe. Similarly, in the Middle East, providers like Khazna Data Centers are scaling up, with new facilities planned to support hyperscale requirements. These expansions reflect a strategic focus on capturing market share in both developed and emerging EMEA markets, driven by increased business investments and product innovation.

Government Initiatives and Regulatory Support

Government policies are fostering market growth through incentives and regulatory frameworks. In 2023, France reduced tariffs on energy for data centers, encouraging further investment. Switzerland’s Federal Act on Data Protection (FADP), aligned with GDPR, bolstered investor confidence by ensuring robust data privacy standards. In the Middle East, Saudi Arabia’s USD 18 billion plan to build a national network of hyperscale data centers, announced prior to 2023 but actively progressing, continues to drive regional growth. These initiatives create a favorable environment for colocation providers, particularly in regions prioritizing digital infrastructure.

UK Market Growth

The UK is emerging as a prime location for colocation services, driven by advancements in ICT infrastructure. In 2023, the telecom sector’s growth, exemplified by Vodafone’s rising brand value, increased demand for data center professional services. Government-backed initiatives to enhance digital infrastructure are expected to sustain this momentum, positioning the UK as a key market through 2028.

Rapid Growth in the Middle East

The Middle East is witnessing accelerated market expansion, supported by strategic investments. In 2023, Saudi Arabia advanced its digital infrastructure goals, with local firms like Gulf Data Hub and Al-Moammar Information Systems contributing to hyperscale facility development. The adoption of 5G services by telecom providers across the region further drives demand for colocation, supporting smart city projects and digital economies in countries like the UAE and Qatar.

Sustainability and Renewable Energy Focus

Sustainability is a growing priority, with colocation providers investing in renewable energy solutions. In 2023, the EMEA region saw increased adoption of solar and other renewable energy sources to power data centers, driven by stringent environmental regulations and initiatives like Saudi Arabia’s Vision 2030, which emphasizes renewable energy integration. These efforts align with regional sustainability goals and enhance market appeal.

Competitive Landscape

Key players, including Equinix, Digital Realty, and Khazna Data Centers, dominate through strategic expansions and acquisitions. New entrants like Agility and EDGNEX Data Centres by DAMAC are disrupting the market, leveraging existing customer bases to drive revenue. In 2023, these providers focused on hyperscale and sustainable facilities to meet evolving demands.

The full report can be found here at: https://www.researchandmarkets.com/reports/6113767/europe-middle-east-africa-emea-data-center (not affiliated).